April 7, 2020

The Bureau of Labor Statistics today released the results of the Job Openings and Labor Turnover Survey (JOLTS) for February. While these data reflect economic conditions prior to the collapse of U.S. labor markets in March, they offer interesting insights into how quickly conditions have deteriorated in U.S. labor markets in the last two weeks.

One of the bellwether statistics that can be calculated using the JOLTS release is how many unemployed individuals there are for every job opening in the U.S. economy. In February, the number of unemployed individuals was 5.787 million and the number of job openings was 6.882 million. This implied a ratio of 0.84 unemployed persons for every job opening, reflecting a very strong labor market, with a February unemployment rate of 3.5 percent.

How does this ratio behave during downturns? Throughout most of 2007, just prior to the Great Recession, the ratio held steady at 1.4-1.5 unemployed individuals for every job opening. When the Great Recession started in December 2007, the ratio was 1.7, but it increased rapidly over 2018, and by January 2009 it had reached 4.4. It continued to increase over the next several months and hit a peak of 6.4 in July of that year.

Given the surge in initial claims for unemployment insurance in the last two weeks, how high was this ratio in March? As I discussed last Friday, the unemployment level reported in the March job report did not fully reflect the collapse of U.S. labor markets in March, as the numbers were based on a reference period just prior to the surge in UI claims.

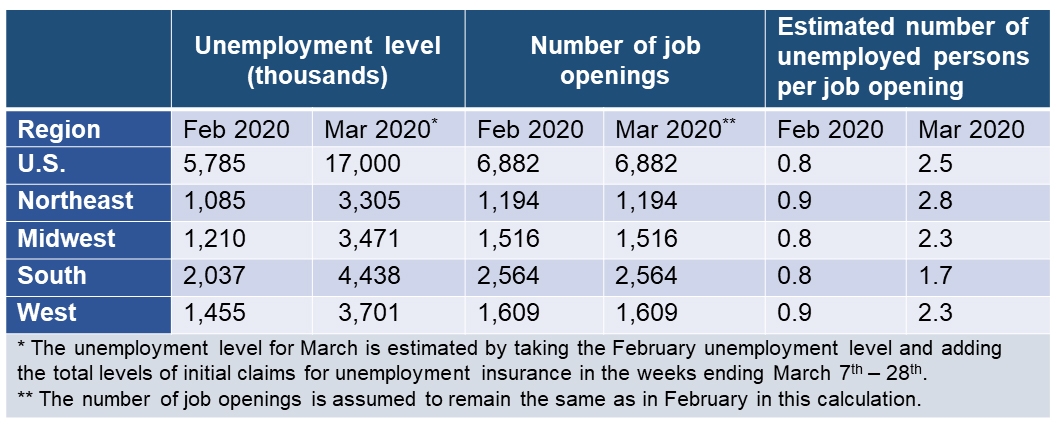

BLS reported that there were 7.1 million people unemployed for the reference week of Sunday, March 8 through Saturday, March 14. If we add the 9.96 million in initial claims for unemployment insurance for the weeks ending March 21 and March 28, that gives an estimate of 17 million unemployed. This is likely an understatement of the total level as it excludes workers who did not file for UI, those whose claims were not yet processed due to backlogs, job loss among the self-employed or additions to unemployment after March 28. Under the very conservative assumption that the number of job openings stayed the same between February and March at 6.9 million—in reality, it almost certainly fell—the ratio of unemployed workers to job openings tripled from 0.8 to 2.5 in just one month! In contrast, it took six months for the ratio to increase from 1.7 to 2.4 at the beginning of the Great Recession. Using our estimated ratio, the chart now has a clear spike that signals the impact of just the last few weeks.

The JOLTS release also provides job openings in February across the four Census regions: Northeast, Midwest, South, and West. The most recent unemployment data for regions is also for February. However, initial claims for unemployment insurance by state (and thus, after aggregating, for region) are available for the weeks ending March 7th through March 28th. The table below conducts a similar exercise as above, but for regions, and finds an analogous spike in the ratio of unemployed individuals per job opening in each region.

Clearly, we are in a very unusual period for U.S. labor markets, one that demands significant policy responses to address the impact of these conditions on our economy and on every individual in our society. The Upjohn Institute has compiled multiple proposals to address the economic hardships resulting from the current pandemic below:

More COVID-19 crisis coverage

Experts